Always look for information on the Gov.UK website.

23rd June 2020 Webinar 9.45-10.30 This was excellent. Below is my transcription:

HMRC updates webinars are regularly updated: visit gov.uk

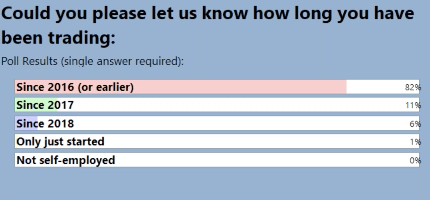

David and Laura from HMRC managed the presentation: they started with a poll:

82 % have been trading before 2016, 1%% since 2017, 6% 2018 Just started 1%

Laura began with the aims of the public service delivered through HMRC:

Support through the disruption

She explained the aim of the scheme

Who can claim

How much

How it’s delivered

What happens when you apply

What support is available if you don’t qualify

Examples: 4 Case Studies

The Aim Of The Scheme

To support the self employed and those in partnerships who’ve been adversely affected. If you’re affected HMRC are delivering a grant support where you can claim 80 % of your average month’s trading profits. (This is capped at £ 7,500 for the three month period covered for the first grant).

The scheme has now been extended continues for companies newly affected by corona virus

The first grant opened 13th May and closes 13th July. You need to apply on or before this date to receive the first grant.

Noone else can claim. If someone else claims on your behalf (for example your financial advisor, tax advisor of accountant or family member, this will trigger a fraud alert and significant delays in processing your application. Please contact HMRC if you are in this category. HMRC have rejected tens of thousands of claims submitted by agents

If the application is successful it will be paid in single instalment.

The first grant application process will close on 14th July. Claims for the first grant should have been made by the 13th July.

Applications for the second grant will open in August 2020.

Eligible people will receive second grant which is for 70%. It will be paid in single instalment 3 months of profits capped at £6,570 in total

Eligibility will be the same as the first grant confirm that business has been adversely affected by Corona Virus or Covid 19 on or after 14th July 2020

Self employed businesses and partnerships can claim second grant even if they didn’t make a claim for the first grant.

Always look for information on the Gov.UK website.

HMRC online service for the second grant will be available soon will publish updated guidance

Who can apply?

Rules the same for both grants

1 Claim if you’re a self employed individual or member of business partnership and you have been adversely affected by corona virus/Covid 19 (or your supply chain has been affected).

2 Claim if you traded in tax year 2018/2019 and you submitted self assessment tax return for that tax year on or before 23rd April 2020

You need to have traded in the tax year 2019/2020 and you were trading when you apply or had temp stopped trading because of Corona Virus and you’re intending to continue to trade in 2020/2021

Also if you have profits of £50,000 equal to non trading income for 2018, or the average of the tax years 2016/2017/ 2017/2018/2018/2019

Don’t apply if you’re a limited company or operating a trade through a trust

List of reasons of adverse effects of Corona Virus:

You’re shielding

Self isolating

On sick leave

Have caring responsibilities

Other reasons (this will be something you’ll have logged that will be apparent through your activity from the beginning of this year and since March)

Have you had to scale down?

Has your supply chain been interrupted? Do you have fewer customers/clients?

Have you been affected by staff not being able to come into work?

HMRC: To determine eligibility we will look at 2018/2019 Tax Return

Trading profits must be no more than £50,000 and must be at least equal to your non trading income.

However, if you’re not eligible 2018/2019

HMRC will look across the previous years

How much will you be entitled to?

The grant is based on an average of three years up to 2018/2019

The first grant will pay 80 per cent single instalment (capped at £7,500)

The second grant from August will pay 70% of average trading profits 3 months capped at £6,570 in total.

As for the first grant you must confirm your business has been adversely affected.

HMRC will work out profits and entitlement based on the information it already has.

If you started 2016-2019 HMRC will base assessment on the self assessments that have already been submitted: If you haven’t submitted self assessment tax returns for all three years HMRC will base average trading profit and entitlement on continuous periods of self employment.

If you’ve been continuously self employed since 2016 HMRC will add together all profits, divide by three, then divide by 12 months in a year to get the average.

If you started in 2017-2018 2018-2019 the average will be divided by 12 over the two tax years.

If you started in 2018-2019 HMRC will use this year only and divide by 12 to get average.

If you traded in 2016 2017 and 2018 2019 only will use and didn’t trade 2017-2018 HMRC will only use one year and divide by 12.

This grant is taxable with deductions for tax and national insurance etc and should be shown as taxable income.

These grants are income for the purposes of other benefits if you claim either of these might be taken into consideration need to say you’re working 16 hours a week.

Examples: 80% £7,500 cap

HMRC first example: Ben a full time self employed florist average profits for 2016-2017-2017-2018-2018-2019.

Ben is eligible: his trading profits are equal to non trading income. His only income from self employment is £18,000. His trading profits create an average of no more than £50,000

For the first taxable grant of monthly trading profits there’s a £7,500 cap

Average trading profits: self employed trading profit 2016-2017: £17,500 2017-2018 £18750 2018-2019 £17750 add total TP £54,000. To get the average divide by 3 =£18,000 then adjust for the 80% = £14,400. The next step divide £14,400 by 12 £1200 per month and then multiply by 3.

How much does Ben receive? It will be the lower of 80 % of ave profit £3,600 set against the maximum grant for the three months of £7,500 lower of two figures, which is the £3,600 figure.

Second example: Nicole is a taxi driver in London. Her average trading profits are £30,000 2016-2018-19. Nicole is eligible as her trading profits are equal to her non trading income income from self employment is again averaged. Nicole’s trading profit is no more than £50,000 Nicole’s first grant calculation trading profits are £30,000 x 80% which is £24,000. Divide this by 12 mnths: £2000 x three months = £6,000. How much will she be eligible for? £6000 which is on the basis of the calculation or £7,500. Whichever is the lowest so Nicole will receive a £6,000 HMRC grant for the three months.

Rashma is an actor. Her trading profits are: 2016-2017 £35,000 2017-2018-£35,000 2018-2019 51,000 (plus 10,00 dividend income). In 2018-2019 Rashma’s trading profit was more than £50,000 but she is eligible because her average trading profit is no more than £50,000 Rashma’s annual trading profits are equal to her non trading income. To get the average divide £121,000 by 3: £40, 334 divide by 80% = £30,268. The next step is to divide by 12 and you get £2689, then multiply by three £8,067 which is more than the threshold of £7,500 for the maximum full grant amount so the amount to be paid will be the lower figure of £7,500.

The fourth case study is Gabriella who’s in partnership with her spouse, selling goods online. Gabriella’s share of profits from partnership is £40,000. Her trading profit in 2018-2019 and £5000 savings make Gabriella is eligible as her non trading income is at least equal to her partnership profits of £40,000. Gabriella’s partnership profits are less than £50,000. The average profits £40,000 x 80% are £32,000. The next step is to divide by 12 =£2667 x 3 to get the average: £8001. How much will Gabriella be entitled to? It’ll be the lowest figure in a comparison of her average £8001 and the threshold figure of £7,500, so in this case Gabriella receives £7,500.

HMRC will work this out

How to claim

Applications for the first grant of the SEISS scheme will close 13th July. To be eligible you must make your first claim by this date.

The government has decided to extend the scheme and the second grant will be available from August.

HMRC has already contacted people based on their tax returns. If you haven’t heard, please use the claim tool on gov.uk

When you claim you need to have:

UTR (Unique Taxpayer reference number), your national insurance number. If after using the tool you’re eligible then sign into your Govt Gateway account (at this point you can create a gateway identity if you don’t have one.

Do this claim on your own account advisors can help but it’s your claim

The eligibility checker will advise reasons why you’re not eligible and let you know how to access other support

You can discuss with HMRC advisor by webchat you can ask for a further review

If you can’t receive a grant there are other forms of help.

Your agent can advise you if you’re eligible HMRC will show you how it’s calculated so you can discuss it further.

If not eligible your agent can rquest a review.

If you are digitally excluded you’ll be invited to contact HMRC an advisor will make the claim on your behalf. If you know someone you think is digitally excluded contact HMRC.

There’s an increase in scams/phishing if asked to give info do not respond: don’t click on links

Any suspiscious emails please send to phishing at hmrc dot gov dot uk

60599 to text

After you apply, if approved the grant will be paid in a single instalment within six days into your account.

If you’ve claimed and haven’t received your grant and it’s over six working days please contact HMRC

Other support is available

The government is providing additional help so you have been able to delay vat and self assessment payments.

You can pay your self assessment in instalments by January 2021.

You might be eligible for a small business grant.

Or be able to apply for a business interruption/bounce back loan.

You may be able to claim Universal Credit or ESA Please go to gov.uk for info

You can defer self assessment payments due in July 2020 until Jan 2021. You don’t need to tell HMRC and they won’t penalise you unless you default and haven’t paid by the end of January 2021.

In relation to VAT: there’s been a deferral from March paymentsuntil 30th Jun 2020.

This defer VAT option ends 30th June 2020 when it must be paid in full and on time. If you haven’t deferred there’s no further action needed. Reinstate DD if you’ve had the payment holiday now as soon as possible. You need to give three days notice.

Resources

You must be logged in to post a comment.